What happens if you die without a will

by Tim Duncan – Compliance Assurance Manager

Last updated 4th April 2025 by the SunLife Content Team

6 min read

If you die without a will – known as 'dying intestate' – the law determines what happens to your estate.

This means there's a risk that loved ones who aren't directly related to you (like a partner or step-child) won't be recognised. The only way to dictate who should inherit your estate is to make a will.

So, what exactly happens if you die without having made a will? Let's take a look.

On this page:

- What does intestacy mean?

- Intestacy rules in England and Wales

- Intestacy rules in Scotland

- Intestacy rules in Northern Ireland

- Applying for a probate when there's no will

- Do I need a will?

- Where to get help

What does intestacy mean?

When you die without a legally valid will, it means you've died 'intestate'. So your estate (which is your money, possessions and property) is shared out according to the rules of intestacy.

Intestacy law varies depending on whether you were married, single or had children. The rules also vary in different parts of the UK.

Intestacy rules in England and Wales

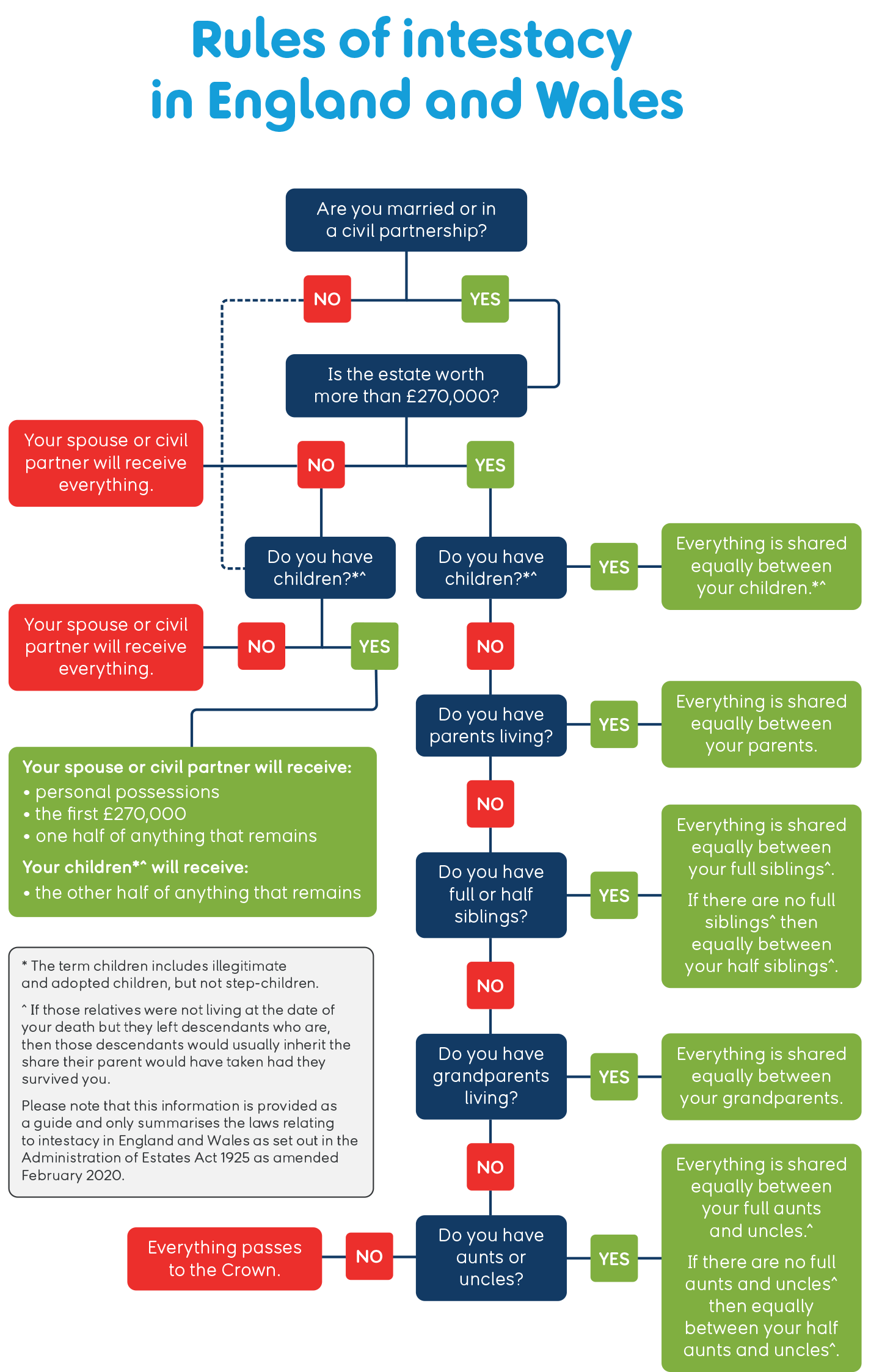

To keep things simple, we've made a chart that shows the rules of intestacy in England and Wales. Take a look to see what could happen to your estate if you died without having made a will.

Here's what happens to your estate if you don't make a will (England and Wales):

Image titled Rules of Intestacy in England and Wales. The data points for the flow chart are as follows:

- Are you married or in a civil partnership? No. Do you have children?*^ Yes. Your spouse or civil partner will receive: personal possessions, the first £270,000, one half of anything that remains. Your children*^ will receive: the other half of anything that remains.

- Are you married or in a civil partnership? No. Do you have children?*^ No. Your spouse or civil partner will receive everything.

- Are you married or in a civil partnership? Yes. Is the estate worth more than £270,000? No. Your spouse or civil partner will receive everything.

- Are you married or in a civil partnership? Yes. Is the estate worth more than £270,000? Yes. Do you have children?*^ Yes. Everything is shared equally between your children.*^

- Are you married or in a civil partnership? Yes. Is the estate worth more than £270,000? Yes. Do you have children?*^ No. Do you have parents living? Yes. Everything is shared equally between your parents.

- Are you married or in a civil partnership? Yes. Is the estate worth more than £270,000? Yes. Do you have children?*^ No. Do you have parents living? No. Do you have full or half siblings? Yes, Everything is shared equally between your full siblings^. If there are no full siblings^ then equally between your half siblings^.

- Are you married or in a civil partnership? Yes. Is the estate worth more than £270,000? Yes. Do you have children?*^ No. Do you have parents living? No. Do you have full or half siblings? No. Do you have grandparents living? Yes. Everything is shared equally between your grandparents.

- Are you married or in a civil partnership? Yes. Is the estate worth more than £270,000? Yes. Do you have children?*^ No. Do you have parents living? No. Do you have full or half siblings? No. Do you have grandparents living? No. Do you have aunts or uncles? Yes. Everything is shared equally between your full aunts and uncles^. If there are no full aunts and uncles^ then equally between your half aunts and uncles^.

- Are you married or in a civil partnership? Yes. Is the estate worth more than £270,000? Yes. Do you have children?*^ No. Do you have parents living? No. Do you have full or half siblings? No. Do you have grandparents living? No. Do you have aunts or uncles? No. Everything passes to the crown.

* The term children includes illegitimate and adopted children, but not step-children.

^If those relatives were not living at the date of your death but they left descendants who are, then those descendants would usually inherit the share their parent would have taken had they survived you.

Please note that this information is provided as a guide and only summarises the laws relating to intestacy in England and Wales as set out in the Administration of Estates Act 1925 as amended February 2020.

If you didn't make a will before you died, who your next of kin is depends on whether you were married and had children.

It's worth remembering that if you're not married or in a civil partnership with your partner, you're single in the eyes of the law – even if you have children and have lived together for years.

So a will is the only way to make sure your surviving partner will inherit your estate.

Order of inheritance

If you died intestate in England or Wales, the following would be the order of inheritance of your estate:

- Spouse or civil partner

- Children/grandchildren

- Parents

- Brothers and sisters

- Grandparents

- Uncles and aunts

('Children' includes illegitimate and adopted children, but not step-children.)

If you're married or in a civil partnership

If your estate is valued at less than £270,000, your spouse or civil partner will inherit everything.

If it's worth more, who gets what will depend on the overall value of your estate. It will also depend on whether you have any other surviving close relatives (like parents, children, siblings or grandchildren).

Anything over £325,000 may be subject to inheritance tax(www.gov.uk opens in a new tab).

Here's how an estate worth over £270,000 could be divided up:

If you have children

Your spouse or civil partner will get:

- Your personal possessions

- The first £270,000 of your estate

- Half of anything left over

Your children will get the other half of anything left over.

If you don't have children

If you don't have any children, your spouse or civil partner will inherit everything.

If you're single and have children

If you have surviving children but aren't married or in a civil partnership, your estate will be divided equally between your children.

Your partner (and any of their children from a previous relationship) won't be entitled to anything.

If your children aren't alive when you die, your grandchildren or other descendants will inherit.

If you're single and don't have children

If you're not married or in a civil partnership and don't have children, your estate will be shared equally between your next closest blood relatives.

These are, in order of priority:

- Parents – not step-parents

- Siblings^ – if you don't have full siblings, your half-siblings

- Grandparents – not step-grandparents

- Aunts or uncles^ – if you don't have full aunts or uncles, your half-aunts or uncles

- First cousins

If you don't have any blood relatives, your estate is passed to the Crown. This is known as bona vacantia(www.gov.uk opens in a new tab).

^ If these relatives weren't alive when you died but left descendants who are, then those descendants would usually inherit what their parent would have inherited if they'd survived you.

Intestacy rules in Scotland

Intestacy law is slightly different in Scotland(www.gov.scot opens in a new tab), where a spouse or civil partner has 'prior rights'.

If there are children:

Your spouse or civil partner will get:

- A share in the family home up to £473,000 as long as it's in Scotland and they live there when you die

- Furniture and household items up to £29,000

- Up to £50,000 in cash

- A third of the rest of the estate

The children will get two-thirds of the rest of the estate.

If there are no children:

Your spouse or civil partner will get:

- Up to £473,000 of the house value

- Furniture and household items up to £29,000

- Up to £89,000 in cash

The rest of the estate is then split in half between any parents, brothers or sisters. Or if they've already died, nieces or nephews will inherit instead.

Intestacy rules in Northern Ireland

Dying intestate in Northern Ireland is different if the person who has died was married or in a civil partnership.

If the deceased was married or in a civil partnership, then they will receive all of the estate up to £250,000.

If the estate is worth over £250,000, then the spouse or civil partner receives £250,000 and personal items.

They will also receive some of the remainder of the estate depending on how many children the deceased has.

If there are no children, the spouse or civil partner gets personal items, the first £450,000 and half of the remainder of the estate. The deceased's parents will get the other half – or if no surviving parents, the deceased's siblings.

For more information on the rules in Northern Ireland, visit the official government website(www.nidirect.co.uk opens in a new tab).

What happens to a jointly owned property when there's no will?

When you own a property with someone else, it will either be as 'tenants in common' or 'joint tenants'.

If you own your house as joint tenants, the property itself isn't counted as part of your estate. So, if one of you dies, the other will automatically inherit their share (even if there's no will).

But, if you share the house as tenants in common and one of you dies, that share of the property won't be automatically inherited. Unless there's a will to say who it should go to, it will be subject to intestacy rules.

Who can't inherit when there's no will?

If you didn't make a will, your estate can't be left to anyone who isn't a blood relative, or who you weren't in a legally-recognised relationship with (like a marriage, civil partnership or adoption).

This includes:

- Unmarried partners – also known as common law partners. Even if you were together for years and had children, an unmarried partner won't automatically inherit if there's no will

- Relations by marriage – e.g. step-children, parents-in-law, brothers or sisters-in-law

- Close friends

However, anyone who believes they should be included in the will can apply to the Court to make a financial claim against the estate.

Applying for a probate when there's no will

People usually name an executor in their will, which means this person has a 'grant of probate'. This gives them legal permission to deal with the deceased's estate after they die.

But, if there's no will and an executor wasn't named, an administrator will need to be appointed to deal with the estate.

This is why having a will is so important – it allows you to appoint someone you trust.

If your loved one dies without a will and you want to be the administrator, you'll have to apply to the Probate Registry(www.gov.uk opens in a new tab).

This means you'll have to get the estate valued, complete an application form (plus other relevant forms), swear an oath and pay a probate fee.

Do I need a will?

The short answer is yes. A will is the only way to make sure your estate will be shared as per your wishes.

While no one really likes to talk about what happens when we die, making a will can ease the burden on your loved ones when the time comes.

Where to get help

There are lots of helpful resources online that explain the ins and outs of making a will and why it matters.

Citizens Advice has a guide to dying intestate(www.citizensadvice.org.uk opens in a new tab). While Gov.uk lays out everything you need to know about intestacy(www.gov.uk opens in a new tab), inheritance tax(www.gov.uk opens in a new tab) and applying for a probate(www.gov.uk opens in a new tab) in England and Wales.

Northern Ireland(www.nidirect.gov.uk opens in a new tab) has slightly different intestacy rules, as does Scotland(www.gov.scot opens in a new tab).

Of course, dealing with the death of a loved one can be distressing. Organisations such as Cruse(opens in a new tab) are here to help support you emotionally and practically.

The information in this website is provided for general guidance only. To ensure you are receiving the best advice, you should contact a specialist advisor.

The thoughts and opinions expressed in the page are those of the authors, intended to be informative, and do not necessarily reflect the official policy or position of SunLife. See our Terms of Use for more info.